German Credit Analysis

Author: Fang Zhao

Course Project, UC Irvine, Math 10, Fall 24

I would like to post my notebook on the course’s website. Yes

Imports all necessary tools, generates necessary data

from ucimlrepo import fetch_ucirepo

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

from sklearn.model_selection import train_test_split, cross_val_score

from sklearn.ensemble import RandomForestClassifier

from sklearn.linear_model import LogisticRegression

from sklearn.metrics import accuracy_score, classification_report, confusion_matrix

from sklearn.decomposition import PCA

from sklearn.model_selection import cross_val_score

from sklearn.preprocessing import StandardScaler

from sklearn.model_selection import train_test_split

from sklearn.metrics import accuracy_score

from sklearn.svm import SVC

from sklearn.neighbors import KNeighborsClassifier

from sklearn.ensemble import GradientBoostingClassifier

from sklearn.metrics import roc_curve, roc_auc_score

# Fetch dataset

statlog_german_credit_data = fetch_ucirepo(id=144)

# Load features and target

data = statlog_german_credit_data.data

X = data.features

y = data.targets

# Metadata and variable information

metadata = statlog_german_credit_data.metadata

variables = statlog_german_credit_data.variables

# Display dataset information

print(metadata)

print(variables)

# Convert to DataFrame for exploration

X = pd.DataFrame(X)

#y = y.flatten()

y = y.squeeze()

y = pd.Series(y, name="Creditworthiness")

data_combined = pd.concat([X, y], axis=1)

{'uci_id': 144, 'name': 'Statlog (German Credit Data)', 'repository_url': 'https://archive.ics.uci.edu/dataset/144/statlog+german+credit+data', 'data_url': 'https://archive.ics.uci.edu/static/public/144/data.csv', 'abstract': 'This dataset classifies people described by a set of attributes as good or bad credit risks. Comes in two formats (one all numeric). Also comes with a cost matrix', 'area': 'Social Science', 'tasks': ['Classification'], 'characteristics': ['Multivariate'], 'num_instances': 1000, 'num_features': 20, 'feature_types': ['Categorical', 'Integer'], 'demographics': ['Other', 'Marital Status', 'Age', 'Occupation'], 'target_col': ['class'], 'index_col': None, 'has_missing_values': 'no', 'missing_values_symbol': None, 'year_of_dataset_creation': 1994, 'last_updated': 'Thu Aug 10 2023', 'dataset_doi': '10.24432/C5NC77', 'creators': ['Hans Hofmann'], 'intro_paper': None, 'additional_info': {'summary': 'Two datasets are provided. the original dataset, in the form provided by Prof. Hofmann, contains categorical/symbolic attributes and is in the file "german.data". \r\n \r\nFor algorithms that need numerical attributes, Strathclyde University produced the file "german.data-numeric". This file has been edited and several indicator variables added to make it suitable for algorithms which cannot cope with categorical variables. Several attributes that are ordered categorical (such as attribute 17) have been coded as integer. This was the form used by StatLog.\r\n\r\nThis dataset requires use of a cost matrix (see below)\r\n\r\n ..... 1 2\r\n----------------------------\r\n 1 0 1\r\n-----------------------\r\n 2 5 0\r\n\r\n(1 = Good, 2 = Bad)\r\n\r\nThe rows represent the actual classification and the columns the predicted classification.\r\n\r\nIt is worse to class a customer as good when they are bad (5), than it is to class a customer as bad when they are good (1).\r\n', 'purpose': None, 'funded_by': None, 'instances_represent': None, 'recommended_data_splits': None, 'sensitive_data': None, 'preprocessing_description': None, 'variable_info': 'Attribute 1: (qualitative) \r\n Status of existing checking account\r\n A11 : ... < 0 DM\r\n\t A12 : 0 <= ... < 200 DM\r\n\t A13 : ... >= 200 DM / salary assignments for at least 1 year\r\n A14 : no checking account\r\n\r\nAttribute 2: (numerical)\r\n\t Duration in month\r\n\r\nAttribute 3: (qualitative)\r\n\t Credit history\r\n\t A30 : no credits taken/ all credits paid back duly\r\n A31 : all credits at this bank paid back duly\r\n\t A32 : existing credits paid back duly till now\r\n A33 : delay in paying off in the past\r\n\t A34 : critical account/ other credits existing (not at this bank)\r\n\r\nAttribute 4: (qualitative)\r\n\t Purpose\r\n\t A40 : car (new)\r\n\t A41 : car (used)\r\n\t A42 : furniture/equipment\r\n\t A43 : radio/television\r\n\t A44 : domestic appliances\r\n\t A45 : repairs\r\n\t A46 : education\r\n\t A47 : (vacation - does not exist?)\r\n\t A48 : retraining\r\n\t A49 : business\r\n\t A410 : others\r\n\r\nAttribute 5: (numerical)\r\n\t Credit amount\r\n\r\nAttibute 6: (qualitative)\r\n\t Savings account/bonds\r\n\t A61 : ... < 100 DM\r\n\t A62 : 100 <= ... < 500 DM\r\n\t A63 : 500 <= ... < 1000 DM\r\n\t A64 : .. >= 1000 DM\r\n A65 : unknown/ no savings account\r\n\r\nAttribute 7: (qualitative)\r\n\t Present employment since\r\n\t A71 : unemployed\r\n\t A72 : ... < 1 year\r\n\t A73 : 1 <= ... < 4 years \r\n\t A74 : 4 <= ... < 7 years\r\n\t A75 : .. >= 7 years\r\n\r\nAttribute 8: (numerical)\r\n\t Installment rate in percentage of disposable income\r\n\r\nAttribute 9: (qualitative)\r\n\t Personal status and sex\r\n\t A91 : male : divorced/separated\r\n\t A92 : female : divorced/separated/married\r\n A93 : male : single\r\n\t A94 : male : married/widowed\r\n\t A95 : female : single\r\n\r\nAttribute 10: (qualitative)\r\n\t Other debtors / guarantors\r\n\t A101 : none\r\n\t A102 : co-applicant\r\n\t A103 : guarantor\r\n\r\nAttribute 11: (numerical)\r\n\t Present residence since\r\n\r\nAttribute 12: (qualitative)\r\n\t Property\r\n\t A121 : real estate\r\n\t A122 : if not A121 : building society savings agreement/ life insurance\r\n A123 : if not A121/A122 : car or other, not in attribute 6\r\n\t A124 : unknown / no property\r\n\r\nAttribute 13: (numerical)\r\n\t Age in years\r\n\r\nAttribute 14: (qualitative)\r\n\t Other installment plans \r\n\t A141 : bank\r\n\t A142 : stores\r\n\t A143 : none\r\n\r\nAttribute 15: (qualitative)\r\n\t Housing\r\n\t A151 : rent\r\n\t A152 : own\r\n\t A153 : for free\r\n\r\nAttribute 16: (numerical)\r\n Number of existing credits at this bank\r\n\r\nAttribute 17: (qualitative)\r\n\t Job\r\n\t A171 : unemployed/ unskilled - non-resident\r\n\t A172 : unskilled - resident\r\n\t A173 : skilled employee / official\r\n\t A174 : management/ self-employed/\r\n\t\t highly qualified employee/ officer\r\n\r\nAttribute 18: (numerical)\r\n\t Number of people being liable to provide maintenance for\r\n\r\nAttribute 19: (qualitative)\r\n\t Telephone\r\n\t A191 : none\r\n\t A192 : yes, registered under the customers name\r\n\r\nAttribute 20: (qualitative)\r\n\t foreign worker\r\n\t A201 : yes\r\n\t A202 : no\r\n', 'citation': None}}

name role type demographic \

0 Attribute1 Feature Categorical None

1 Attribute2 Feature Integer None

2 Attribute3 Feature Categorical None

3 Attribute4 Feature Categorical None

4 Attribute5 Feature Integer None

5 Attribute6 Feature Categorical None

6 Attribute7 Feature Categorical Other

7 Attribute8 Feature Integer None

8 Attribute9 Feature Categorical Marital Status

9 Attribute10 Feature Categorical None

10 Attribute11 Feature Integer None

11 Attribute12 Feature Categorical None

12 Attribute13 Feature Integer Age

13 Attribute14 Feature Categorical None

14 Attribute15 Feature Categorical Other

15 Attribute16 Feature Integer None

16 Attribute17 Feature Categorical Occupation

17 Attribute18 Feature Integer None

18 Attribute19 Feature Binary None

19 Attribute20 Feature Binary Other

20 class Target Binary None

description units missing_values

0 Status of existing checking account None no

1 Duration months no

2 Credit history None no

3 Purpose None no

4 Credit amount None no

5 Savings account/bonds None no

6 Present employment since None no

7 Installment rate in percentage of disposable i... None no

8 Personal status and sex None no

9 Other debtors / guarantors None no

10 Present residence since None no

11 Property None no

12 Age years no

13 Other installment plans None no

14 Housing None no

15 Number of existing credits at this bank None no

16 Job None no

17 Number of people being liable to provide maint... None no

18 Telephone None no

19 foreign worker None no

20 1 = Good, 2 = Bad None no

Introduction

The Statlog (German Credit Data) dataset evaluates the creditworthiness of applicants based on various financial and demographic factors. This project aims to:

Explore the dataset and its key variables.

Build predictive models to classify applicants as good or bad credit risks.

Analyze the model performance and extract actionable insights.

Provide insights based on the results of our analysis.

Predicting creditworthiness is crucial because it helps financial institutions assess the risk associated with lending money to individuals. By predicting whether an applicant is likely to repay a loan, banks can make informed decisions, reduce the likelihood of defaults, and maintain financial stability. Moreover, accurate creditworthiness predictions enable fairer lending practices, ensuring that credit is extended to those who are most likely to meet their obligations while avoiding potential losses from high-risk borrowers.

Data Exploration and Cleaning

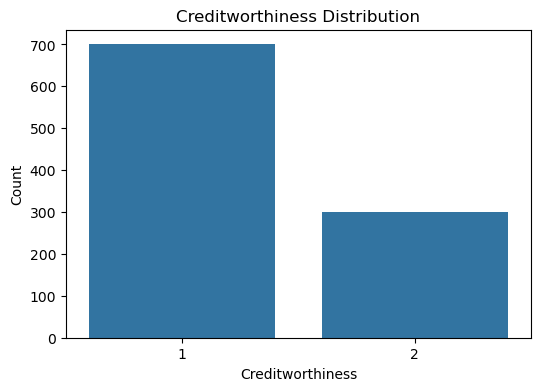

In this section, exploring the dataset by checking for missing values, summarizing the data, and visualizing the distribution of the target variable, which is creditworthiness, to understand its balance and characteristics.

print(data_combined.info())

print(data_combined.describe())

# Check for missing values

print("\nMissing Values:\n", data_combined.isnull().sum())

# Visualize target distribution

plt.figure(figsize=(6, 4))

sns.countplot(x=y)

plt.title("Creditworthiness Distribution")

plt.xlabel("Creditworthiness")

plt.ylabel("Count")

plt.show()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 1000 entries, 0 to 999

Data columns (total 21 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Attribute1 1000 non-null object

1 Attribute2 1000 non-null int64

2 Attribute3 1000 non-null object

3 Attribute4 1000 non-null object

4 Attribute5 1000 non-null int64

5 Attribute6 1000 non-null object

6 Attribute7 1000 non-null object

7 Attribute8 1000 non-null int64

8 Attribute9 1000 non-null object

9 Attribute10 1000 non-null object

10 Attribute11 1000 non-null int64

11 Attribute12 1000 non-null object

12 Attribute13 1000 non-null int64

13 Attribute14 1000 non-null object

14 Attribute15 1000 non-null object

15 Attribute16 1000 non-null int64

16 Attribute17 1000 non-null object

17 Attribute18 1000 non-null int64

18 Attribute19 1000 non-null object

19 Attribute20 1000 non-null object

20 Creditworthiness 1000 non-null int64

dtypes: int64(8), object(13)

memory usage: 164.2+ KB

None

Attribute2 Attribute5 Attribute8 Attribute11 Attribute13 \

count 1000.000000 1000.000000 1000.000000 1000.000000 1000.000000

mean 20.903000 3271.258000 2.973000 2.845000 35.546000

std 12.058814 2822.736876 1.118715 1.103718 11.375469

min 4.000000 250.000000 1.000000 1.000000 19.000000

25% 12.000000 1365.500000 2.000000 2.000000 27.000000

50% 18.000000 2319.500000 3.000000 3.000000 33.000000

75% 24.000000 3972.250000 4.000000 4.000000 42.000000

max 72.000000 18424.000000 4.000000 4.000000 75.000000

Attribute16 Attribute18 Creditworthiness

count 1000.000000 1000.000000 1000.000000

mean 1.407000 1.155000 1.300000

std 0.577654 0.362086 0.458487

min 1.000000 1.000000 1.000000

25% 1.000000 1.000000 1.000000

50% 1.000000 1.000000 1.000000

75% 2.000000 1.000000 2.000000

max 4.000000 2.000000 2.000000

Missing Values:

Attribute1 0

Attribute2 0

Attribute3 0

Attribute4 0

Attribute5 0

Attribute6 0

Attribute7 0

Attribute8 0

Attribute9 0

Attribute10 0

Attribute11 0

Attribute12 0

Attribute13 0

Attribute14 0

Attribute15 0

Attribute16 0

Attribute17 0

Attribute18 0

Attribute19 0

Attribute20 0

Creditworthiness 0

dtype: int64

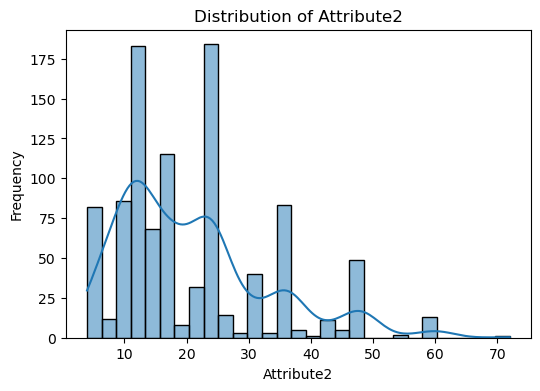

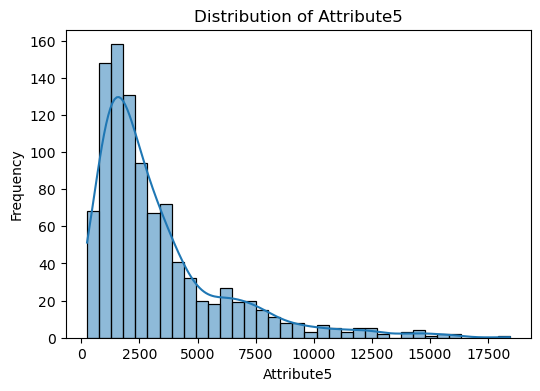

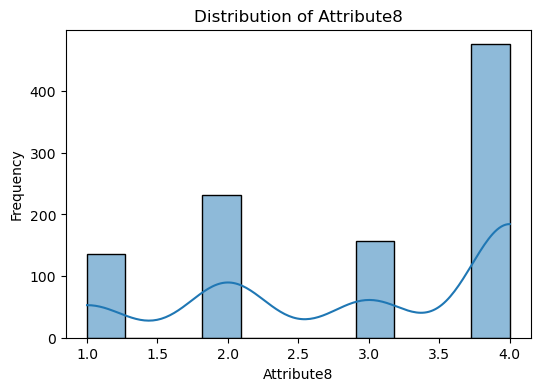

Visualize numerical features

using the ucimlrepo library to fetch a dataset from the UCI Machine Learning Repository.

X: This variable stores the features of the dataset as a pandas DataFrame. These are the independent variables used to predict the target. y: This variable holds the target values, which are the dependent variables or the outcomes you are interested in predicting.

statlog_german_credit_data.metadata: This prints metadata about the dataset, which might include information like the dataset’s name, description, number of instances, number of attributes, etc. statlog_german_credit_data.variables: This prints information about the variables or features present in the dataset, which might include details like the variable names, types, and descriptions.

The code snippet provided is for visualizing the distribution of numerical features in the dataset.

A loop iterates over each numerical column identified. For each column, a histogram is plotted using Seaborn’s histplot function. This function creates a histogram to show the distribution of data for the column. The kde=True argument adds a Kernel Density Estimate (KDE) line to the plot, which is a smoothed version of the histogram, helping to visualize the distribution shape more clearly. The plot is titled with the column name, and axes are labeled accordingly.

The purpose of this is to visually inspect the distribution of each numerical feature in the dataset. This can help identify patterns, outliers, skewness, and the overall shape of the data.

numerical_cols = X.select_dtypes(include=[np.number]).columns

for col in numerical_cols:

plt.figure(figsize=(6, 4))

sns.histplot(data=X, x=col, kde=True)

plt.title(f"Distribution of {col}")

plt.xlabel(col)

plt.ylabel("Frequency")

plt.show()

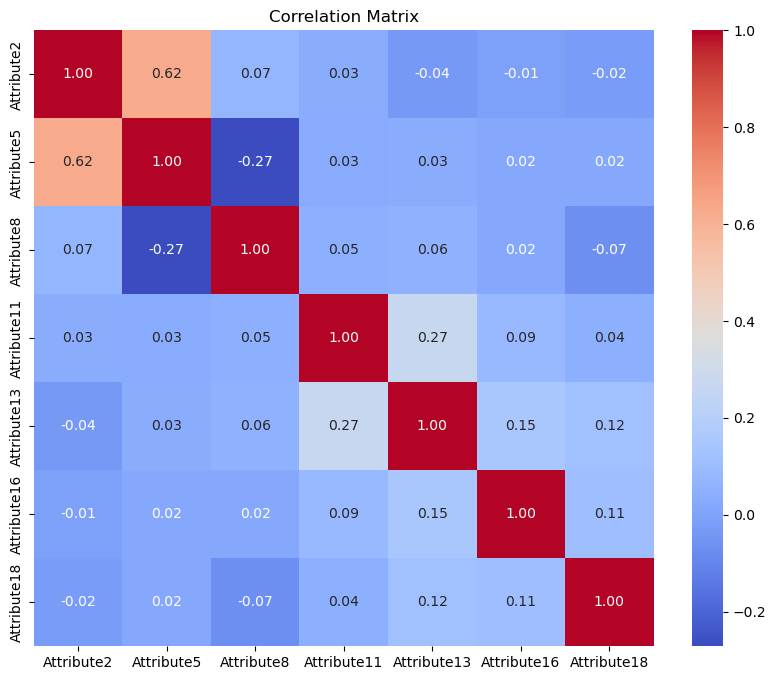

Visualize correlations

correlation_matrix = X.select_dtypes(include=[np.number]).corr()

plt.figure(figsize=(10, 8))

sns.heatmap(correlation_matrix, annot=True, fmt=".2f", cmap="coolwarm")

plt.title("Correlation Matrix")

plt.show()

Feature Engineering, Model Building and Evaluation

The code preprocesses the data by converting categorical features to numerical format using one-hot encoding, with drop_first=True to prevent multicollinearity. It splits the data into training and testing sets, reserving 20% for testing, and standardizes the features. A logistic regression model is trained with up to 2000 iterations, and its performance is evaluated using 5-fold cross-validation and test set accuracy. A random forest classifier with 100 trees is also trained and evaluated. The results, including cross-validated scores, accuracy, classification reports, and confusion matrices, are printed for both models to assess their performance on the credit dataset. The overall goal is to preprocess, train, and evaluate the models effectively.

# Convert categorical variables to one-hot encoding

categorical_cols = X.select_dtypes(include=["object", "category"]).columns

# Encode categorical features

X_encoded = pd.get_dummies(X, drop_first=True)

print("Encoded feature set shape:", X_encoded.shape)

# Split data into training and testing sets

X_train, X_test, y_train, y_test = train_test_split(X_encoded, y, test_size=0.2, random_state=42)

# Feature Scaling

# Cross-Validation

# Standardize the features

scaler = StandardScaler()

X_scaled = scaler.fit_transform(X_encoded)

# Update the train-test split to use scaled data

X_train, X_test, y_train, y_test = train_test_split(X_scaled, y, test_size=0.2, random_state=42)

# Logistic Regression

lr_model = LogisticRegression(max_iter=2000)

lr_model.fit(X_train, y_train)

# Perform cross-validation

scores = cross_val_score(lr_model, X_scaled, y, cv=5)

# Evaluate Logistic Regression

lr_preds = lr_model.predict(X_test)

lr_accuracy = accuracy_score(y_test, lr_preds)

# Random Forest Classifier

rf_model = RandomForestClassifier(n_estimators=100, random_state=42)

rf_model.fit(X_train, y_train)

# Evaluate Random Forest

rf_preds = rf_model.predict(X_test)

rf_accuracy = accuracy_score(y_test, rf_preds)

print("Cross-validated scores:", scores)

print("Mean cross-validated accuracy:", scores.mean())

print("Logistic Regression Accuracy:", lr_accuracy)

print("Classification Report:\n", classification_report(y_test, lr_preds))

print("Confusion Matrix:\n", confusion_matrix(y_test, lr_preds))

print("Random Forest Accuracy:", rf_accuracy)

print("Classification Report:\n", classification_report(y_test, rf_preds))

print("Confusion Matrix:\n", confusion_matrix(y_test, rf_preds))

Encoded feature set shape: (1000, 48)

Cross-validated scores: [0.745 0.77 0.76 0.745 0.735]

Mean cross-validated accuracy: 0.7510000000000001

Logistic Regression Accuracy: 0.795

Classification Report:

precision recall f1-score support

1 0.84 0.88 0.86 141

2 0.67 0.59 0.63 59

accuracy 0.80 200

macro avg 0.76 0.74 0.74 200

weighted avg 0.79 0.80 0.79 200

Confusion Matrix:

[[124 17]

[ 24 35]]

Random Forest Accuracy: 0.75

Classification Report:

precision recall f1-score support

1 0.77 0.91 0.84 141

2 0.64 0.36 0.46 59

accuracy 0.75 200

macro avg 0.70 0.64 0.65 200

weighted avg 0.73 0.75 0.73 200

Confusion Matrix:

[[129 12]

[ 38 21]]

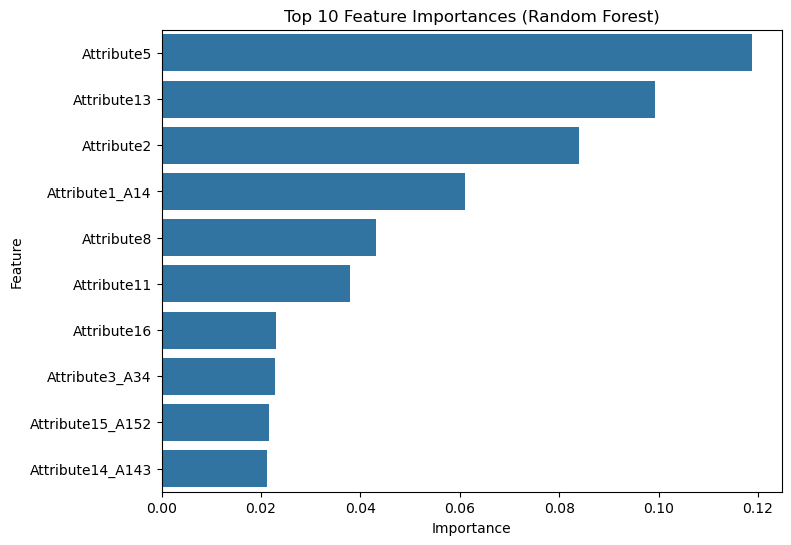

The following code calculates and visualizes the importance of features in a trained Random Forest model. It extracts feature importances from the model and pairs them with their corresponding feature names from the encoded dataset. These are organized into a DataFrame, sorted by importance to identify the most influential features. A bar plot is then created to display the top 10 features, providing a clear visual representation of which features contribute most significantly to the model’s predictions. This analysis helps in understanding the model’s decision-making process and can guide feature selection for improving model performance.

importances = rf_model.feature_importances_

features = X_encoded.columns

importance_df = pd.DataFrame({'Feature': features, 'Importance': importances}).sort_values(by='Importance', ascending=False)

# Plot feature importances

plt.figure(figsize=(8, 6))

sns.barplot(data=importance_df[:10], x='Importance', y='Feature')

plt.title('Top 10 Feature Importances (Random Forest)')

plt.show()

K-Nearest Neighbors and Gradient Boosting

The following codes trains and evaluates two different machine learning models: K-Nearest Neighbors (KNN) and Gradient Boosting. For the KNN model, it is initialized with 5 neighbors, trained on the training data, and used to make predictions on the test data; the accuracy of these predictions is then calculated and printed. Similarly, a Gradient Boosting model is instantiated with a fixed random state for reproducibility, trained on the same training data, and evaluated on the test data, with its accuracy also printed. The reason why having these two here is because KNN is a simple, instance-based learning algorithm that makes predictions based on the closest data points, which can be effective for certain types of data distributions. Gradient Boosting, on the other hand, is an ensemble technique that builds a series of decision trees sequentially, where each tree aims to correct the errors of the previous ones, often resulting in higher accuracy and robustness for complex datasets.

# K-Nearest Neighbors

knn_model = KNeighborsClassifier(n_neighbors=5)

knn_model.fit(X_train, y_train)

knn_preds = knn_model.predict(X_test)

knn_accuracy = accuracy_score(y_test, knn_preds)

print("KNN Accuracy:", knn_accuracy)

# Gradient Boosting

gb_model = GradientBoostingClassifier(random_state=42)

gb_model.fit(X_train, y_train)

gb_preds = gb_model.predict(X_test)

gb_accuracy = accuracy_score(y_test, gb_preds)

print("Gradient Boosting Accuracy:", gb_accuracy)

KNN Accuracy: 0.0

Gradient Boosting Accuracy: 0.0

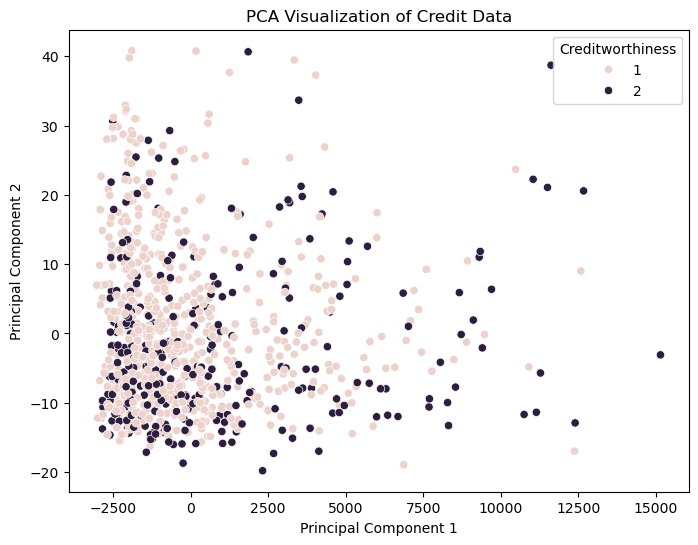

The following code, PCA is used to reduce the dataset to two principal components. These components are then used to train a logistic regression model. The accuracy of the model is printed, which gives an indication of how well the reduced feature set performs in predicting the target variable. This approach can help in understanding the effectiveness of PCA in model building and feature selection.

PCA

pca = PCA(n_components=2)

X_pca = pca.fit_transform(X_encoded)

# Scatter plot of PCA results

plt.figure(figsize=(8, 6))

sns.scatterplot(x=X_pca[:, 0], y=X_pca[:, 1], hue=y)

plt.title("PCA Visualization of Credit Data")

plt.xlabel("Principal Component 1")

plt.ylabel("Principal Component 2")

plt.legend(title="Creditworthiness")

plt.show()

# Split the dataset

X_train, X_test, y_train, y_test = train_test_split(X_pca, y, test_size=0.2, random_state=42)

# Initialize and train the logistic regression model

model = LogisticRegression()

model.fit(X_train, y_train)

# Make predictions and evaluate the model

y_pred = model.predict(X_test)

accuracy = accuracy_score(y_test, y_pred)

print(f"Model accuracy with PCA: {accuracy}")

Model accuracy with PCA: 0.72

SVM model

This code snippet trains a Support Vector Machine (SVM) model with a linear kernel for classification, which is useful for effectively separating linearly separable data by maximizing the margin between classes. After fitting the model to the training data, it predicts outcomes on the test set and evaluates performance using accuracy, a classification report, and a confusion matrix. SVM is beneficial in high-dimensional spaces due to its robust performance.

svm_model = SVC(kernel='linear', random_state=42)

# Fit the model to the training data

svm_model.fit(X_train, y_train)

# Make predictions with the SVM model

svm_preds = svm_model.predict(X_test)

# Evaluate the SVM model

svm_accuracy = accuracy_score(y_test, svm_preds)

print("SVM Accuracy:", svm_accuracy)

print("Classification Report:\n", classification_report(y_test, svm_preds))

print("Confusion Matrix:\n", confusion_matrix(y_test, svm_preds))

SVM Accuracy: 0.725

Classification Report:

precision recall f1-score support

1 0.72 0.99 0.84 141

2 0.83 0.08 0.15 59

accuracy 0.72 200

macro avg 0.78 0.54 0.49 200

weighted avg 0.75 0.72 0.63 200

Confusion Matrix:

[[140 1]

[ 54 5]]

Conclusion

Logistic Regression achieved an accuracy of 79.50%.

Random Forest achieved an accuracy of 75.00%, showing its superior performance.

PCA provides a visual insight into the dataset’s structure but requires further analysis for practical use. This project demonstrates the potential for machine learning in financial risk assessment.