Linear Regression#

Problem#

Given the training dataset \(x_i\in\mathbb{R}\), \(y_i\in\mathbb{R}\), \(i= 1,2,..., N\), we want to find the linear function

that fits the relations between \(x_i\) and \(y_i\). So that given any \(x\), we can make the prediction

Loss Function and Optimization#

With the training dataset, define the loss function \(L(w,b)\) of parameter \(w\) and \(b\), which is also called mean squared error (MSE)

where \(\hat{y}^{(i)}\) denotes the predicted value of y at \(x_i\), i.e. \(\hat{y}^{(i)} = wx_i+b\).

Our goal is to find the optimal \(w\) and \(b\) that minimize the loss function \(L(w,b)\), i.e.

This is a function of \(w\) and \(b\), and we can analytically solve \(\partial_{w}L = \partial_{b}L =0\), and yields

where \(\bar{X}\) and \(\bar{Y}\) are the mean of \(x\) and of \(y\), and \(\text{Cov}(X,Y)\) denotes the estimated covariance (or called sample covariance) between \(X\) and \(Y\), \(\text{Var}(Y)\) denotes the sample variance of \(Y\).

Evaluating the model#

MSE: The smaller MSE indicates better performance.

MSE depends on the unit. For example, if we replace y[m] by y[mm], than MSE will be \(1000^2\) times the original MSE.

\(R^{2}\) (coefficient of determination): The larger \(R^{2}\) (closer to 1) indicates better performance. Compared with MSE, R-squared is dimensionless, not dependent on the units of variable.

Intuitively, MSE is the “unexplained” variance, and \(R^{2}\) is the proportion of the variance that is explained by the model: If our model is perfect, then MSE is 0, and \(R^{2}\) is 1. If we are using a constant model, then our best prediction is the mean of \(y\), and MSE is the variance of \(y\), and \(R^{2}\) is 0;

import numpy as np

import matplotlib.pyplot as plt

class myLinearRegression:

'''

The single-variable linear regression estimator.

This serves as an example of the regression models from sklearn, with methods fit, predict, and score.

'''

def __init__(self):

'''

'''

self.w = None

self.b = None

def fit(self, x, y):

# covariance matrix,

# bias = True makes the factor 1/N, otherwise 1/(N-1)

# but it doesn't matter here, since the factor will be cancelled out in the calculation of w

cov_mat = np.cov(x, y, bias=True)

# cov_mat[0, 1] is the covariance of x and y, and cov_mat[0, 0] is the variance of x

self.w = cov_mat[0, 1] / cov_mat[0, 0]

self.b = np.mean(y) - self.w * np.mean(x)

# :.3f means 3 decimal places

print(f'w = {self.w:.3f}, b = {self.b:.3f}')

def predict(self, x):

'''

Predict the output values for the input value x, based on trained parameters

'''

ypred = self.w * x + self.b

return ypred

def score(self, x, y):

'''

Calculate the R^2 score of the model

'''

mse = np.mean((y - self.predict(x))**2)

var = np.mean((y - np.mean(y))**2)

Rsquare = 1 - mse / var

return Rsquare

# Generate synthetic data

np.random.seed(0) # for reproducibility

a = 0

b = 2

N = 20

x = np.random.uniform(a,b,N)

y = 2 * x + 1 + np.random.randn(N)

y_gt = 2 * x + 1

# Fit the model

lm = myLinearRegression()

lm.fit(x, y)

score = lm.score(x, y)

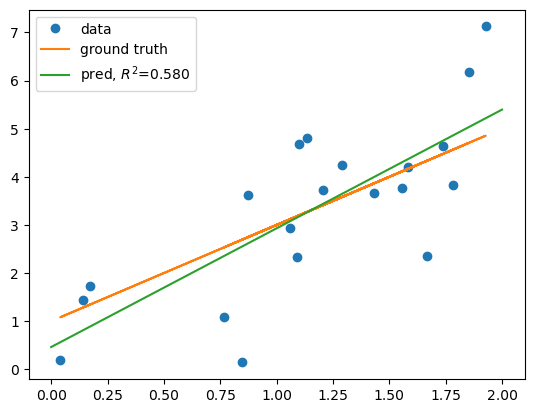

# plot data

plt.plot(x, y, 'o', label='data')

# plot ground truth

plt.plot(x, y_gt, label='ground truth')

# plot the linear regression model

xs = np.linspace(a, b, 100)

plt.plot(xs, lm.predict(xs), label=f'pred, $R^2$={score:.3f}')

plt.legend()

print(f'score = {score:.3f}')

w = 2.467, b = 0.462

score = 0.580

We can also use LinearRegression from sklearn.linear_model to fit the linear model.

# Use the following command to install scikit-learn

# %conda install scikit-learn

# or

# %pip install scikit-learn

from sklearn.linear_model import LinearRegression

reg = LinearRegression()

# x need to be n-sample by p features

reg.fit(x.reshape(-1, 1), y)

print(f'w = {reg.coef_[0]:.3f}, b = {reg.intercept_:.3f}')

score = reg.score(x.reshape(-1, 1), y)

print(f'score = {score:.3f}')

w = 2.467, b = 0.462

score = 0.580

What is the effect of centering the data?#

When \(X\) is centered, the slope \(w\) remains the same, but the intercept \(b\) changes.

The intercept now means the predicted Y when X is at the mean.

x_center = x - np.mean(x)

reg.fit(x_center.reshape(-1, 1), y)

print(f'w = {reg.coef_[0]:.3f}, b = {reg.intercept_:.3f}')

w = 2.467, b = 3.332

When Y is centered, then the intercept \(b\) is 0, and the slope \(w\) is the correlation between \(X\) and \(Y\).

y_center = y - np.mean(y)

reg.fit(x_center.reshape(-1, 1), y_center)

print(f'w = {reg.coef_[0]:.3f}, b = {reg.intercept_:.3f}')

w = 2.467, b = 0.000

What is the effect of scaling the data?#

When \(X/c\) is used, the optimal slope is now \(c w\), and the intercept does not change

# suppose we want to scale x to [0, 1]

scale_factor = np.max(x)

x_scale = x / scale_factor

reg.fit(x_scale.reshape(-1, 1), y)

print(f'w = {reg.coef_[0]:.3f}, b = {reg.intercept_:.3f}')

w = 4.756, b = 0.462

For linear regression, centering and scaling the data (both training and testing data ) does not affect the performance of the model.

For some other models, centering and scaling can be essential

Appendix#

Detailed Derivation of the Optimal Parameters (Not exam material).

The loss function for simple linear regression is given by:

To find the optimal ( w ), we set the partial derivative of ( L ) with respect to ( w ) to zero:

Differentiate with respect to ( w ):

Rearrange this equation to get:

Derivative with respect to \(b\):

This simplifies to:

Or, equivalently:

Substitute \(b\) back into the equation (*), we get:

Expanding this:

Rearranging terms

Now, solving for \(w\):

Recall that \(Cov(X,Y) = E[XY]-E[X]E[Y]\), and \(Var(X) = E[X^2] - E[X]^2\). Divide both the numerator and the denominator by \(N\). We can rewrite the above equation in terms of covariance and variance: $\(w = \frac{Cov(X,Y)}{Var(X)}\)$

This is the final expression for \(w^*\) in simple linear regression, representing the slope of the best-fit line.