Automatic loan verification#

Author: Elijah Jacobs

Course Project, UC Irvine, Math 10, Spring 25

I would like to post my notebook on the course’s website. Yes

Introduction#

In this project I will work on a dataset regarding loan dispersement and ideally make a model to classify a loan as able to be dispersed or not. I am focusing on this because as a student with loans, I would like to know how the whole process might be able to be modeled using regression and classification methods we learned in class.

The dataset that I will be using was found on Kaggle, I will post the link under this paragraph. It includes many factors that may go into consideration for a loan and holds 45,000 instances each with 14 variables of interest.

https://www.kaggle.com/datasets/taweilo/loan-approval-classification-data

Features:#

person_age: Age of the person in years

person_gender: Gender of the person

person_education: Highest education level

person_income: Annual income in dollars

person_emp_exp: Years of employment experience

person_home_ownership: Home ownership status (e.g., rent, own, mortgage)

loan_amnt: Loan amount requested in dollars

loan_intent: Purpose of the loan

loan_int_rate: Loan interest rate

loan_percent_income: Loan amount as a percentage of annual income

cb_person_cred_hist_length: Length of credit history in years

credit_score: Credit score of the person

previous_loan_defaults_on_file: Indicator of previous loan defaults

loan_status: Loan approval status: 1 = approved; 0 = rejected This is our target variable

# importing all the important libraries required

from sklearn.model_selection import train_test_split

import sklearn.linear_model as lin

from sklearn.metrics import confusion_matrix

from sklearn.preprocessing import OneHotEncoder

import torch

from torch.utils.data import Dataset

import torch.nn as nn

import torch.optim as optim

from torch.utils.data import DataLoader

import seaborn as sns

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

Now I will load the data set and drop any na values if there are any

df = pd.read_csv('loan_data.csv')

df.dropna(inplace=True)

df

| person_age | person_gender | person_education | person_income | person_emp_exp | person_home_ownership | loan_amnt | loan_intent | loan_int_rate | loan_percent_income | cb_person_cred_hist_length | credit_score | previous_loan_defaults_on_file | loan_status | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 22.0 | female | Master | 71948.0 | 0 | RENT | 35000.0 | PERSONAL | 16.02 | 0.49 | 3.0 | 561 | No | 1 |

| 1 | 21.0 | female | High School | 12282.0 | 0 | OWN | 1000.0 | EDUCATION | 11.14 | 0.08 | 2.0 | 504 | Yes | 0 |

| 2 | 25.0 | female | High School | 12438.0 | 3 | MORTGAGE | 5500.0 | MEDICAL | 12.87 | 0.44 | 3.0 | 635 | No | 1 |

| 3 | 23.0 | female | Bachelor | 79753.0 | 0 | RENT | 35000.0 | MEDICAL | 15.23 | 0.44 | 2.0 | 675 | No | 1 |

| 4 | 24.0 | male | Master | 66135.0 | 1 | RENT | 35000.0 | MEDICAL | 14.27 | 0.53 | 4.0 | 586 | No | 1 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 44995 | 27.0 | male | Associate | 47971.0 | 6 | RENT | 15000.0 | MEDICAL | 15.66 | 0.31 | 3.0 | 645 | No | 1 |

| 44996 | 37.0 | female | Associate | 65800.0 | 17 | RENT | 9000.0 | HOMEIMPROVEMENT | 14.07 | 0.14 | 11.0 | 621 | No | 1 |

| 44997 | 33.0 | male | Associate | 56942.0 | 7 | RENT | 2771.0 | DEBTCONSOLIDATION | 10.02 | 0.05 | 10.0 | 668 | No | 1 |

| 44998 | 29.0 | male | Bachelor | 33164.0 | 4 | RENT | 12000.0 | EDUCATION | 13.23 | 0.36 | 6.0 | 604 | No | 1 |

| 44999 | 24.0 | male | High School | 51609.0 | 1 | RENT | 6665.0 | DEBTCONSOLIDATION | 17.05 | 0.13 | 3.0 | 628 | No | 1 |

45000 rows × 14 columns

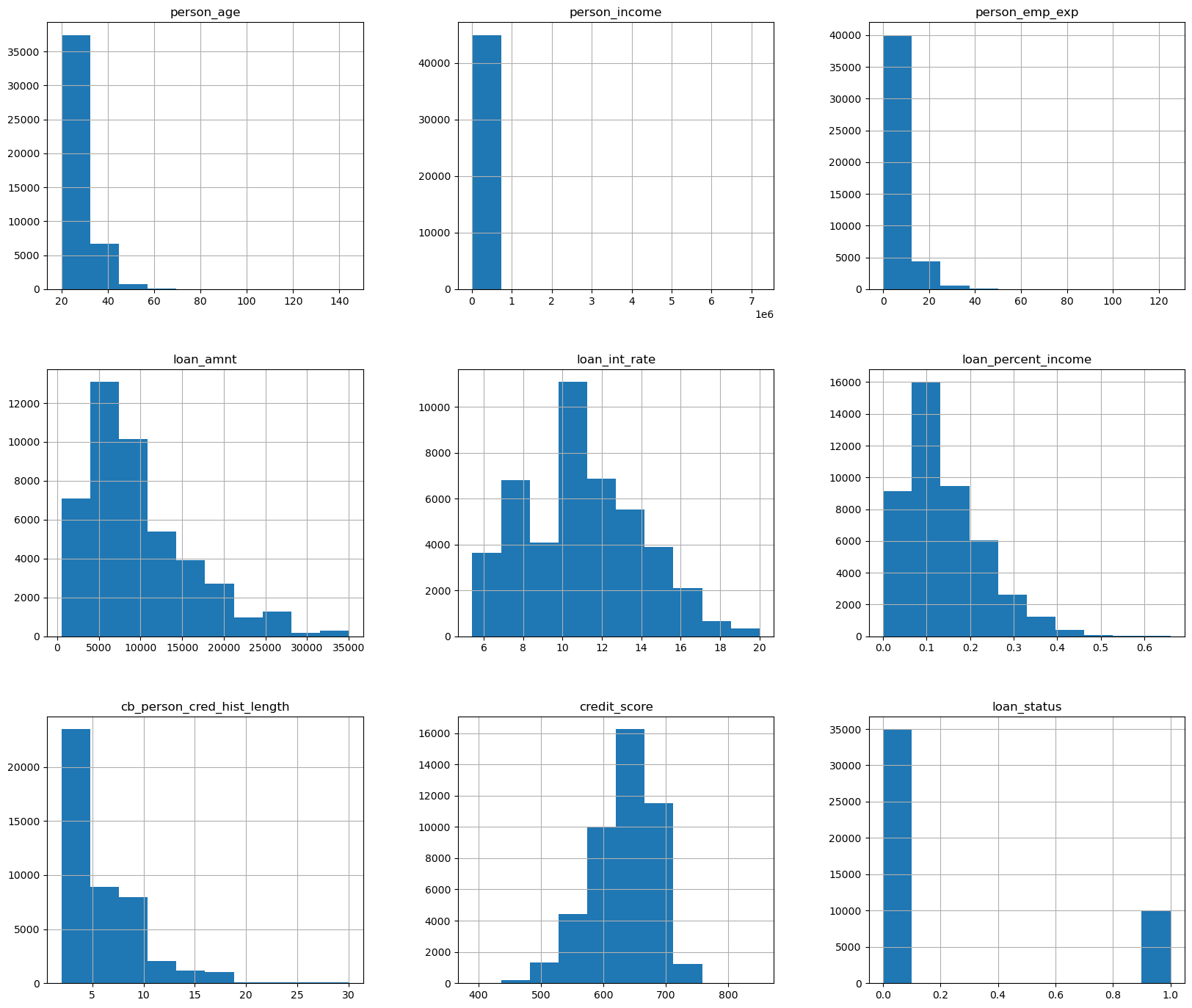

This what the distributions of the data look like

df.hist(figsize=(20,17))

plt.show()

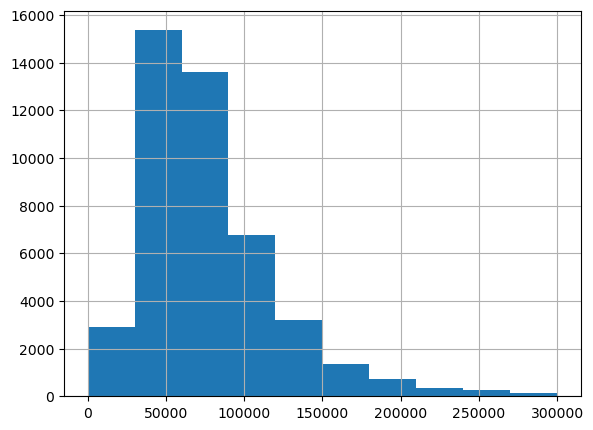

the only histogram here that doesn’t look neat is person_income, so I will graph it again separately so we have an idea of what it looks like.

df['person_income'].hist(figsize=(20/3,20/4),range=(0,300000))

plt.show()

We can see that a lot of our data is roughly normally distributed, allowing us to standardize it as such later when we scale down some of our datav for modeling purposes.

Since previous loan defaults is only made up of yes’s and no’s I am going to change the data there so that yes = 1 and no = 0

I will do the same with gender with 1 as male and 0 as female

# makes it so if previous_loan_defaults_on_file is Yes or 1 or True then it will set it to be True/1 and everything else to False/0

df['previous_loan_defaults_on_file'] = ((df['previous_loan_defaults_on_file'] == 'Yes') | (df['previous_loan_defaults_on_file'] == 1))*1

# makes it so if person_gender is male or 1 or True then it will set it to be True/1 and everything else to False/0

df['person_gender'] = ((df['person_gender'] == 'male') | (df['person_gender'] == 1))*1

print(df['previous_loan_defaults_on_file'])

print(df['person_gender'])

0 0

1 1

2 0

3 0

4 0

..

44995 0

44996 0

44997 0

44998 0

44999 0

Name: previous_loan_defaults_on_file, Length: 45000, dtype: int32

0 0

1 0

2 0

3 0

4 1

..

44995 1

44996 0

44997 1

44998 1

44999 1

Name: person_gender, Length: 45000, dtype: int32

In order to use the categorical data I am going to use the one-hot-encoder method where we will have new features based on the classifications of things like gender and education, where each row will be either a 1 or a 0 in each of the new features depending on what classification they belong to.

code flows from https://www.geeksforgeeks.org/ml-one-hot-encoding/

catagories = ['person_education', 'person_home_ownership', 'loan_intent']

# make OneHotEncoder object

OHE = OneHotEncoder(sparse_output=False)

# apply object to our categorical data

newcata = OHE.fit_transform(df[catagories])

# add new features to our dataframe

clean_df = pd.concat([df, pd.DataFrame(newcata, columns=OHE.get_feature_names_out(catagories), index=df.index)], axis=1)

# drop original categories

clean_df.drop(columns=catagories, inplace=True)

clean_df

| person_age | person_gender | person_income | person_emp_exp | loan_amnt | loan_int_rate | loan_percent_income | cb_person_cred_hist_length | credit_score | previous_loan_defaults_on_file | ... | person_home_ownership_MORTGAGE | person_home_ownership_OTHER | person_home_ownership_OWN | person_home_ownership_RENT | loan_intent_DEBTCONSOLIDATION | loan_intent_EDUCATION | loan_intent_HOMEIMPROVEMENT | loan_intent_MEDICAL | loan_intent_PERSONAL | loan_intent_VENTURE | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 22.0 | 0 | 71948.0 | 0 | 35000.0 | 16.02 | 0.49 | 3.0 | 561 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 |

| 1 | 21.0 | 0 | 12282.0 | 0 | 1000.0 | 11.14 | 0.08 | 2.0 | 504 | 1 | ... | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 2 | 25.0 | 0 | 12438.0 | 3 | 5500.0 | 12.87 | 0.44 | 3.0 | 635 | 0 | ... | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 |

| 3 | 23.0 | 0 | 79753.0 | 0 | 35000.0 | 15.23 | 0.44 | 2.0 | 675 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 |

| 4 | 24.0 | 1 | 66135.0 | 1 | 35000.0 | 14.27 | 0.53 | 4.0 | 586 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 44995 | 27.0 | 1 | 47971.0 | 6 | 15000.0 | 15.66 | 0.31 | 3.0 | 645 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 |

| 44996 | 37.0 | 0 | 65800.0 | 17 | 9000.0 | 14.07 | 0.14 | 11.0 | 621 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 |

| 44997 | 33.0 | 1 | 56942.0 | 7 | 2771.0 | 10.02 | 0.05 | 10.0 | 668 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 44998 | 29.0 | 1 | 33164.0 | 4 | 12000.0 | 13.23 | 0.36 | 6.0 | 604 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 |

| 44999 | 24.0 | 1 | 51609.0 | 1 | 6665.0 | 17.05 | 0.13 | 3.0 | 628 | 0 | ... | 0.0 | 0.0 | 0.0 | 1.0 | 1.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 |

45000 rows × 26 columns

Now that we have our data fixed up we can now get along with trying a classification algorithm.

Classification algorithm#

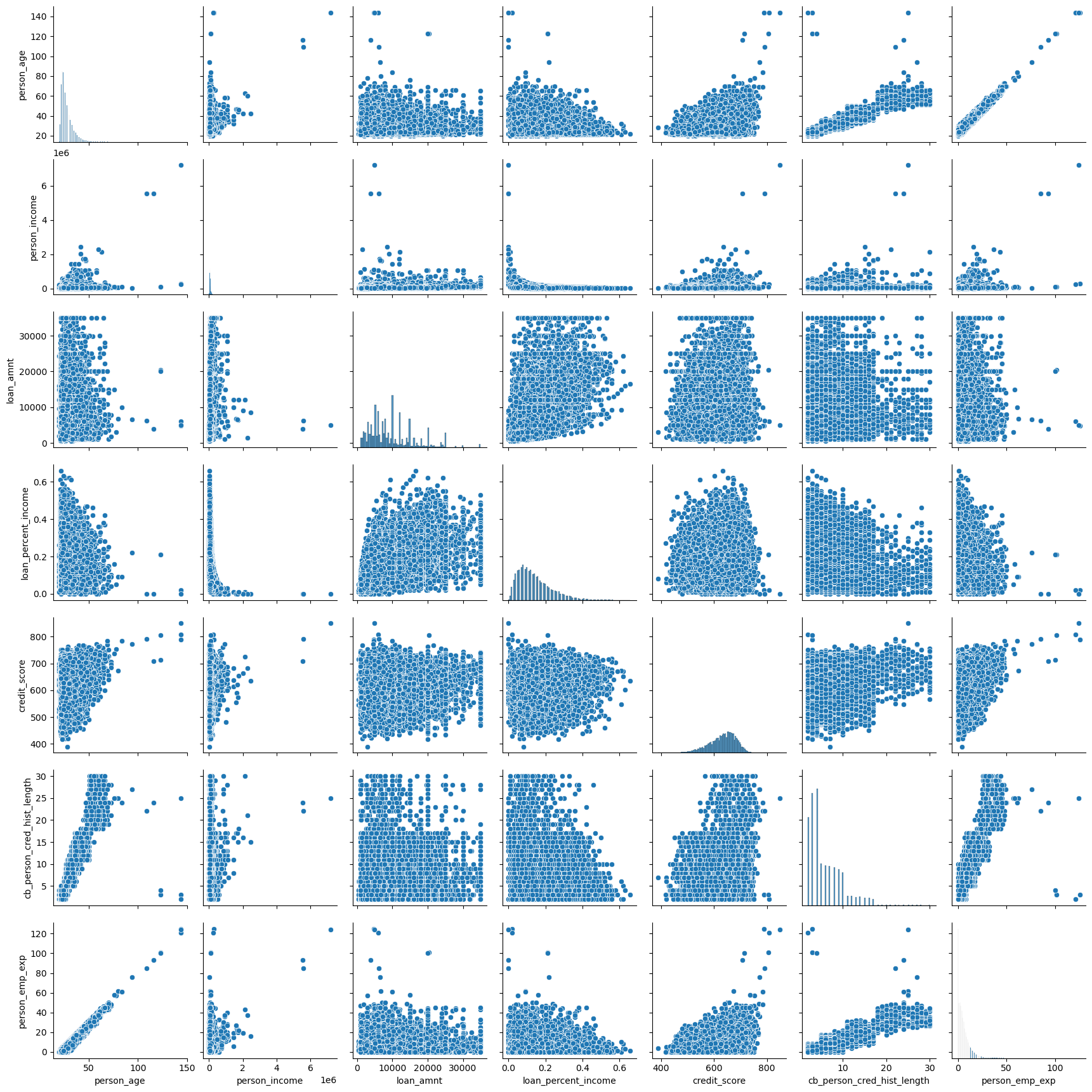

Before using any of the data, I am going to check for what features are colinear and remove them from consideration, however I will not be getting rid of any of the categorical data. First I will graph the scatter plots of all the data, and then I will check the linearity matrix to see what I should remove.

sns.pairplot(df[['person_age', 'person_income', 'loan_amnt', 'loan_percent_income', 'credit_score','cb_person_cred_hist_length','person_emp_exp']], diag_kind='hist')

<seaborn.axisgrid.PairGrid at 0x1ee19994d10>

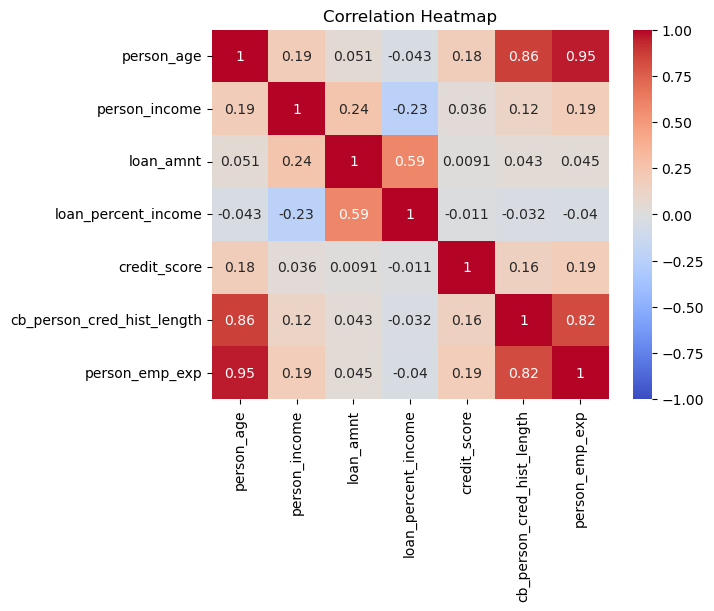

It appears that things like credit history, age, and employment time all correlate pretty highly. We will confirm this notion with a correlation matrix.

correlation_matrix = clean_df[['person_age', 'person_income', 'loan_amnt', 'loan_percent_income', 'credit_score','cb_person_cred_hist_length','person_emp_exp']].corr()

sns.heatmap(correlation_matrix, annot=True, cmap='coolwarm', vmin=-1, vmax=1)

plt.title('Correlation Heatmap')

plt.show()

We are right, and due to the high colinearity between credit history, employment history, and age, I will keep the person’s age and drop the other two columns from the data.

By the way, there is an abundance of data meaning there is no need to use cross validation or folds, I will do a 60-40 split of the data. I will also be scaling the data with regards to a normal distribution so it is easier to train later models.

# defines what columns are to be changed

fixed_df = clean_df.drop(columns=['person_emp_exp', 'cb_person_cred_hist_length'])

columns = ['person_age', 'person_income', 'loan_amnt', 'loan_int_rate', 'credit_score']

# changes columns

for column in columns:

fixed_df[column] =(fixed_df[column] - fixed_df[column].mean() ) / fixed_df[column].std()

# split data into features and targets

df_features = fixed_df.drop(columns='loan_status')

df_target = fixed_df['loan_status']

#split features and targets into testing and training sets

train_features, test_features, train_target, test_target = train_test_split(df_features, df_target, test_size=.4)

I will be trying two different models to see what works best, for starters however I am interested in how well logistic regression does with classifying our data.

Logistic#

# trains logistic model

log = lin.LogisticRegression(max_iter=10000)

log.fit(train_features, train_target)

LogisticRegression(max_iter=10000)In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook.

On GitHub, the HTML representation is unable to render, please try loading this page with nbviewer.org.

LogisticRegression(max_iter=10000)

We will now display the accuracy on the testing and training sets

#tests logistic model, showing it's accuracy

print(f'train acc: {log.score(train_features, train_target)}')

print(f'test acc: {log.score(test_features, test_target)}')

train acc: 0.8952222222222223

test acc: 0.8964444444444445

Both values exceeded my expectations. I thought the model might not be able to fit to such a large dataset, I am happy my worries were missplaced.

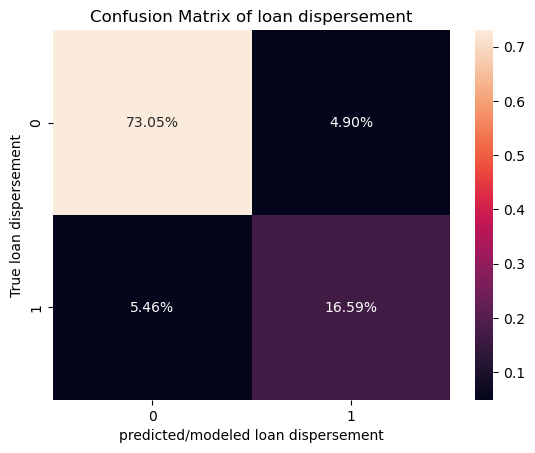

For now I will continue and show the confusion matrix to get a better sense of how well the data is being modeled.

I figured out how to do percentages for the confusion matrix with the website given here: https://medium.com/@dtuk81/confusion-matrix-visualization-fc31e3f30fea

# creates confusion matrix

con = confusion_matrix(test_target, log.predict(test_features))

#creates heatmap of confusion matrix

sns.heatmap(con/np.sum(con), annot=True, xticklabels=[0,1], yticklabels=[0,1], fmt='.2%')

plt.xlabel('predicted/modeled loan dispersement')

plt.ylabel('True loan dispersement')

plt.title('Confusion Matrix of loan dispersement')

plt.show()

Here a 1 means that the loan was dispersed and a 0 means that it was not dispersed. I am quite happy with how logistic regression did at modeling the given data as the accuracy was pretty close to 90% and the false negatives and false positives are pretty equally distributed meaning that the model is giving out a normal amount of loans rather than giving too much or too little. Due to how accurate the model runs on the testing data, there is likely no over-fitting in the model.

Neural Network#

Now that I have tried logistic regression I am interested in how well a neural network will handle the data.

We will use the same split as the previous model.

Credit to both the math10 course website by Professor Zhang, Chad, and the Pytorch website for this next bit

https://rayzhangzirui.github.io/math10sp25/notes/intro_nn.html

https://docs.pytorch.org/tutorials/beginner/basics/buildmodel_tutorial.html

# defining a dataset class to reformat data

class MyDataset(Dataset):

def __init__(self, data, target):

self.data = torch.from_numpy(data)

self.target = torch.from_numpy(target)

def __len__(self):

return len(self.data)

def __getitem__(self, idx):

return self.data[idx], self.target[idx]

# making data sets

train_ds = MyDataset(train_features.astype('float32').values, train_target.values)

test_ds = MyDataset(test_features.astype('float32').values, test_target.values)

batch_size = 100

# Creating dataloaders

train_dataloader = DataLoader(train_ds, batch_size=batch_size)

test_dataloader = DataLoader(test_ds, batch_size=batch_size)

# defining model

layer_size = 20

class NeuralNet(nn.Module):

def __init__(self):

super(NeuralNet, self).__init__()

self.flatten = nn.Flatten()

self.layers = nn.Sequential(

nn.Linear(23, layer_size),

nn.Sigmoid(),

nn.Linear(layer_size, layer_size),

nn.Sigmoid(),

nn.Linear(layer_size, layer_size),

nn.Sigmoid(),

nn.Linear(layer_size, layer_size),

nn.Sigmoid(),

nn.Linear(layer_size, 2)

)

def forward(self, x):

x = self.flatten(x)

logits = self.layers(x)

prob = nn.functional.softmax(logits, dim=1)

return prob

model = NeuralNet()

# making Loss and Optimizer

bceloss = nn.CrossEntropyLoss()

optimizer = optim.Adam(model.parameters(), lr=.005)

# Computes accuracy

def evaluate(loader):

model.eval()

total, correct = 0, 0

with torch.no_grad():

for features, target in loader:

features, target = features, target

outputs = model(features)

_, predicted = torch.max(outputs.data, 1)

total += target.size(0)

correct += (predicted == target).sum().item()

return 100 * correct / total

# Run training through the data 100 times and store values of testing accuracy in a list

n_epoch = 60

acc_list = []

for epoch in range(n_epoch):

model.train()

for features, target in train_dataloader:

features, target = features, target

outputs = model(features)

loss = bceloss(outputs, target)

optimizer.zero_grad()

loss.backward()

optimizer.step()

# gives accuracy of each epoch of the training and testing data

accuracy = evaluate(test_dataloader)

acc_list.append(accuracy)

accuracyT = evaluate(train_dataloader)

print(f'Epoch {epoch+1}, loss: {loss.item():.4f}, training accuracy: {accuracyT:.2f}% test accuracy: {accuracy:.2f}%')

# Evaluate the final accuracy on testing set

final_accuracy = evaluate(test_dataloader)

print(f'Test Accuracy: {final_accuracy:.2f}%')

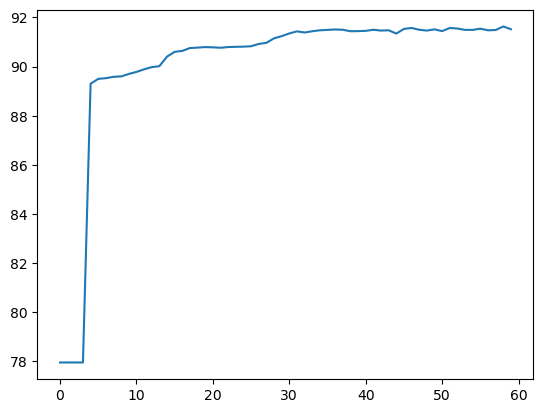

plt.plot(acc_list)

Epoch 1, loss: 0.5932, training accuracy: 77.66% test accuracy: 77.95%

Epoch 2, loss: 0.5932, training accuracy: 77.66% test accuracy: 77.95%

Epoch 3, loss: 0.5932, training accuracy: 77.66% test accuracy: 77.95%

Epoch 4, loss: 0.5911, training accuracy: 77.66% test accuracy: 77.95%

Epoch 5, loss: 0.4063, training accuracy: 89.39% test accuracy: 89.30%

Epoch 6, loss: 0.4017, training accuracy: 89.44% test accuracy: 89.50%

Epoch 7, loss: 0.4042, training accuracy: 89.37% test accuracy: 89.53%

Epoch 8, loss: 0.4057, training accuracy: 89.44% test accuracy: 89.58%

Epoch 9, loss: 0.4069, training accuracy: 89.55% test accuracy: 89.60%

Epoch 10, loss: 0.4079, training accuracy: 89.61% test accuracy: 89.70%

Epoch 11, loss: 0.4083, training accuracy: 89.69% test accuracy: 89.78%

Epoch 12, loss: 0.4082, training accuracy: 89.74% test accuracy: 89.89%

Epoch 13, loss: 0.4075, training accuracy: 89.84% test accuracy: 89.98%

Epoch 14, loss: 0.4067, training accuracy: 89.91% test accuracy: 90.02%

Epoch 15, loss: 0.4050, training accuracy: 90.33% test accuracy: 90.41%

Epoch 16, loss: 0.4045, training accuracy: 90.57% test accuracy: 90.60%

Epoch 17, loss: 0.4071, training accuracy: 90.71% test accuracy: 90.64%

Epoch 18, loss: 0.4109, training accuracy: 90.79% test accuracy: 90.76%

Epoch 19, loss: 0.4138, training accuracy: 90.79% test accuracy: 90.77%

Epoch 20, loss: 0.4150, training accuracy: 90.79% test accuracy: 90.79%

Epoch 21, loss: 0.4152, training accuracy: 90.81% test accuracy: 90.78%

Epoch 22, loss: 0.4150, training accuracy: 90.81% test accuracy: 90.77%

Epoch 23, loss: 0.4145, training accuracy: 90.83% test accuracy: 90.79%

Epoch 24, loss: 0.4137, training accuracy: 90.85% test accuracy: 90.81%

Epoch 25, loss: 0.4125, training accuracy: 90.88% test accuracy: 90.81%

Epoch 26, loss: 0.4094, training accuracy: 90.91% test accuracy: 90.83%

Epoch 27, loss: 0.4059, training accuracy: 91.05% test accuracy: 90.92%

Epoch 28, loss: 0.4031, training accuracy: 91.17% test accuracy: 90.97%

Epoch 29, loss: 0.4007, training accuracy: 91.31% test accuracy: 91.15%

Epoch 30, loss: 0.3995, training accuracy: 91.38% test accuracy: 91.24%

Epoch 31, loss: 0.3976, training accuracy: 91.43% test accuracy: 91.35%

Epoch 32, loss: 0.3985, training accuracy: 91.47% test accuracy: 91.43%

Epoch 33, loss: 0.4001, training accuracy: 91.50% test accuracy: 91.39%

Epoch 34, loss: 0.4023, training accuracy: 91.54% test accuracy: 91.44%

Epoch 35, loss: 0.4050, training accuracy: 91.61% test accuracy: 91.48%

Epoch 36, loss: 0.4080, training accuracy: 91.70% test accuracy: 91.49%

Epoch 37, loss: 0.4040, training accuracy: 91.77% test accuracy: 91.51%

Epoch 38, loss: 0.4119, training accuracy: 91.80% test accuracy: 91.50%

Epoch 39, loss: 0.4144, training accuracy: 91.74% test accuracy: 91.44%

Epoch 40, loss: 0.4130, training accuracy: 91.81% test accuracy: 91.44%

Epoch 41, loss: 0.4065, training accuracy: 91.85% test accuracy: 91.46%

Epoch 42, loss: 0.4066, training accuracy: 91.89% test accuracy: 91.50%

Epoch 43, loss: 0.4119, training accuracy: 91.89% test accuracy: 91.47%

Epoch 44, loss: 0.4025, training accuracy: 91.95% test accuracy: 91.48%

Epoch 45, loss: 0.4085, training accuracy: 91.90% test accuracy: 91.34%

Epoch 46, loss: 0.4142, training accuracy: 91.93% test accuracy: 91.53%

Epoch 47, loss: 0.4033, training accuracy: 92.06% test accuracy: 91.57%

Epoch 48, loss: 0.4133, training accuracy: 92.01% test accuracy: 91.50%

Epoch 49, loss: 0.4121, training accuracy: 92.04% test accuracy: 91.47%

Epoch 50, loss: 0.4075, training accuracy: 92.09% test accuracy: 91.52%

Epoch 51, loss: 0.4055, training accuracy: 92.05% test accuracy: 91.44%

Epoch 52, loss: 0.4057, training accuracy: 92.13% test accuracy: 91.57%

Epoch 53, loss: 0.4065, training accuracy: 92.11% test accuracy: 91.55%

Epoch 54, loss: 0.4050, training accuracy: 92.11% test accuracy: 91.49%

Epoch 55, loss: 0.4012, training accuracy: 92.08% test accuracy: 91.49%

Epoch 56, loss: 0.4044, training accuracy: 92.15% test accuracy: 91.54%

Epoch 57, loss: 0.4068, training accuracy: 92.14% test accuracy: 91.48%

Epoch 58, loss: 0.4094, training accuracy: 92.10% test accuracy: 91.49%

Epoch 59, loss: 0.4017, training accuracy: 92.19% test accuracy: 91.63%

Epoch 60, loss: 0.4024, training accuracy: 92.23% test accuracy: 91.52%

Test Accuracy: 91.52%

[<matplotlib.lines.Line2D at 0x1ee283d2870>]

I initially ran this having not scaled the data to be standardized and was very confused when I was getting consistent values of 77.73% for the accuracy of the model. Now however, I have fixed that and am consistently getting better accuracy than the logistical model at above 91%. Due to how close the testing and training accuracy are to each other there is likely very little over-fitting meaning that are model isn’t too complex, which would’ve caused too much variance in our data due to the bias-variance tradeoff.

From the graph we can see that the model experience’s a large initial increase in accuracy, then it very slowly increases up to about 91%, then the accuracy levels out after about 15-20 epochs.

Regardless, both models appear to accurately depict the loan dispersement data.

Conclusion#

Modeling the dispersement of loans is done effectively through the use of Logistic regression, however the use of neural networks appears to lead to slight improvements in accuracy when compared to the logistical model.

This is all to say that it is possible to make a machine to predict whether or not some was or was not approved for a loan. This can lead to automation in banking, ultimately cutting costs that would normally be paid to human analysts, allowing them to focus more on the overview of these models and perhaps more important issues in banking that they would not have been able to weigh in on initially.

I’d say these models are quite comforting as someone who might need loans later their life. As with a relatively linear relationship, it can be expected that one would need to meet certain specific criteria in order to get a loan, the process of getting one isn’t based completely on luck.